Despite being law in New Zealand for well over a decade, the Personal Property Securities Act 1993 (“PPSA”) remains a mystery to some and misunderstood by many.

The minimal time and costs involved in protecting your interests under the PPSA can make a significant impact when compared to the economic loss you could suffer when the correct procedures have not been followed.

A Brief Background to the PPSA

The PPSA overhauled the pre-existing laws and numerous registers in relation to personal property and introduced a new set of rules relating to security interests in personal property. One of the fundamental changes was to replace the former key concepts of “ownership” and “title” with that of “priority”.

Underpinning the PPSA is the Personal Property Securities Register (“PPSR”). This serves as a public notice board that a party is claiming a security interest in certain assets. This register is online and, being accessible 24/7, it provides real time information about any security registered against an entity.

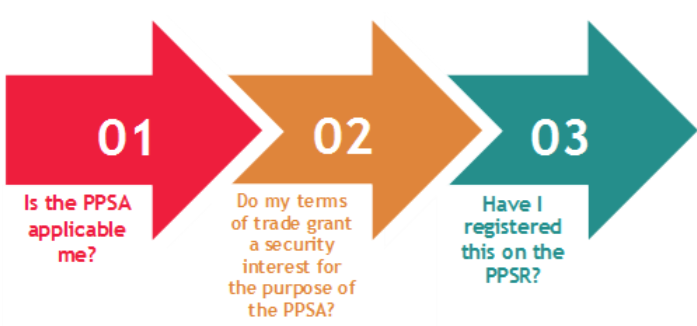

Is the PPSA applicable to me?

Generally, if a business is supplying goods to customers on credit, the PPSA is going to be applicable and the business should be familiar with how it operates.

Terms of trade should include language that reflects the PPSA. At a minimum, there should be a clause in the terms of sale that grants a security interest in any goods supplied for the purpose of the PPSA.

The granting of a security interest should be viewed as the first step that a creditor takes to protect its interest. Although not compulsory, in order to provide any meaningful protection, the

next step should then be to register that interest on the PPSR as soon as possible. This process is completed online, is quick, and at present costs $16.10. Failure to register your security interest may result in a secured party losing priority to other creditors who have registered.

Internal PPSA Processes

Preparing and Understanding Financing Statements

A secured party registers a financing statement on the PPSR. Ensure that you have correctly identified the legal entity you are dealing with. Mistakes made in this respect when registering on the PPSR may render a financing statement invalid or ineffective.

Goods subject to the security interest are termed ‘collateral’. If a secured party is supplying goods on an ongoing basis, it is generally only necessary to register one financing statement, however, be sure the description of the collateral is broad enough to cover all likely future supplies.

Financing statements are valid for five years after which time (if not renewed) they expire and become invalid. Ensure that that if security is still required, the financing statement is renewed before its expiry to ensure continued protection.

Correctly Executed Documents

Ensure that terms and conditions of sale or credit applications are filled in correctly and signed by your customer. It is not uncommon for businesses to provide us with terms of sale that have not been signed or otherwise agreed to.

Easily Accessible Documents

In the event of insolvency, the receiver or liquidator will request to review these documents to ensure the validity of any security interests. Signed terms and conditions should be stored in a secure and easily accessible location.

Dedicated Generic PPSR Email Address

In the event of liquidation or receivership, legislation imposes strict timeframes for secured creditors to respond and make an election in respect of their security. As email is usually the primary mode of communication, we suggest using a generic PPSR email address that is monitored by more than one person. We often find the email address on the PPSR is for an individual no longer employed or on extended leave. A secured creditor who fails to respond to a liquidator’s notice within the requisite timeframe runs the risk of surrendering their security and becoming an unsecured creditor.

What should you do now?

All businesses, especially those supplying goods on credit, should be aware of the provisions and the effect of the PPSR. Failure to register a security interest could have dramatic consequences as to who benefits from the sale of an asset in an insolvent estate.

BDO can undertake a risk review to ensure adequate coverage in the event a client or customer is placed in receivership or liquidation. Some simple and inexpensive checks could save you thousands of dollars.

DISCLAIMER: this article is intended to provide general information about the Personal Property Securities Act 1993. It is not meant to be construed as specific legal, accounting, or insolvency advice.