Equity markets for the year so far can be described in one word: Volatile

The current situation in markets is being driven by rising interest rates, alongside multi-decade high inflation, clogged supply chains and the war in Ukraine.

Times like these can often spark our ‘fight or flight’ instinct, or alternatively investors might avoid any risk altogether. But both scenarios could potentially harm the likelihood of achieving long term investment goals. It highlights the importance of having an investment plan to guide your decision making.

The length of time you look to hold your investments – the ‘time horizon’ – is important, because the approach you take when investing for the long-term may differ to that over a shorter period. This is all dependent on an investor’s unique risk tolerance, investment goals and needs, which are key for investors to clarify from the outset.

Investment returns

Does time really heal everything?

A longer timeline generally means an investor has greater capacity to take on risk, with the ability to withstand short-term drops in value. This allows a plan to be created for a well-constructed, diversified portfolio, which would usually contain a mix of asset classes (e.g., equities/shares, fixed income/bonds, cash) with different levels of investment risk and return.

When assessing an investment risk profile, there are a few key areas we regularly discuss with clients at Jarden; the amount of investable assets available, any cashflow demands, and their investment time horizon. This period ends when they need to draw down capital from their investment portfolio. It’s also important to think about the level of risk an investor is comfortable taking on, as well as any prior investment experience.

In periods of volatility, seeing a real-time decline in your portfolio’s value can be painful. However, conditions change, and any sudden reactions could result in losing potential future gains. Looking at the US equity market daily returns (excluding dividends) from 1927 to 2021, an investor who stayed in the market for all days would have made a 6.1 per cent capital gain (per annum), while those who missed the 25 best days made only 3.5 per cent.

By staying in the markets for longer periods, there is enough time to see them turn.

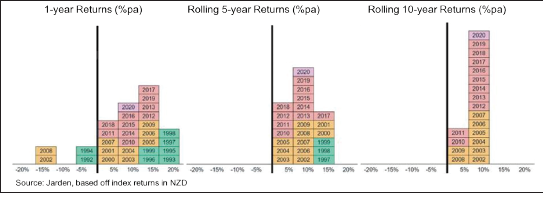

Our wealth research team analysed rolling returns from a sample “Balanced” portfolio (60% growth assets and 40% income assets) classified as medium risk from 1992-2020. It showed over shorter periods of time, the portfolio was exposed to higher risks of negative returns. But over longer periods of time, the portfolio had historically produced positive annual returns on average.

Occasional changes to a portfolio – aligned with investment goals – can be beneficial. However, making decisions in reaction to current events can carry a greater risk of not meeting your aims, and create stress.

The next time an investor thinks about altering their portfolio, they should consider whether today’s situation impacts how their overall investments align with their objectives, or if their goals have changed. Often, it can be best to stay put.