The talk of the town locally is the recent Colliers sale of two iconic office buildings in the heart of central Napier, Dalton and Vautier Houses, heralding an era of extensive redevelopment in Napier CBD and presenting exciting leasing opportunities within the city.

The landmark properties, recognised as the largest office block in the Hawke’s Bay region, were acquired by Wallace Development Company, a move that promises to transform the cityscape and invigorate the commercial landscape.

Boasting a 100 per cent NBS rating, the buildings will feature flexible floorspaces that cater to a range of needs. Wallace Developments will be enclosing balconies to create more floor space, the total net lettable office space will increase from 7,269m² to 8,400m² providing ample room for businesses to thrive.

Other recent sales concluded by Colliers Hawke’s Bay include the vacant possession sale of Simply Squeezed Factory, coolstore and bottling plant situated in Bayview. Simply Squeezed owned by Frucor Suntory decided that the plant at Bay View would be closed and sold after operating for more than 30 years.

A significant industrial asset situated at 39 Edmundson Street, Onekawa, with a lease to Move Logistics has sold for the second time within two years, again reiterating the resilience of the Hawke’s Bay industrial market and lack of available land in Onekawa.

A brand-new NPD self- service fuel station on Heretaunga Street Hastings sold only one week after the doors opened at a yield of 5.82%, not far from where Colliers would have expected this to sell this asset at the peak of the market now 18-24 months ago.

This property had a brand new 15-year lease with annual 2% increases. The sale price shows there is still strong local demand for quality bottom drawn investments with solid tenant covenants.

Stabilisation in interest rate forecasts indicates turn in market activity ahead

The influence of interest rate rises on investor sentiment and sales activity within the commercial and industrial property sector is inescapable, but so too is the potential for growth given the forecasts of peak interest rate hikes this cycle.

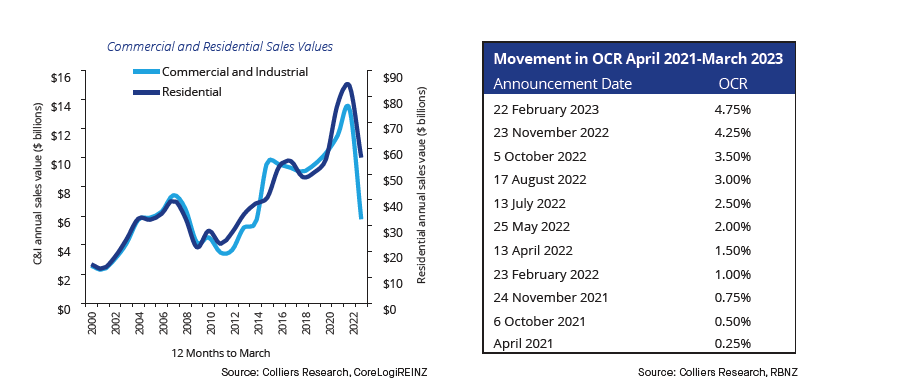

Between April 2021 and March 2022, historically low interest rates, with the Official Cash Rate (OCR) ranging from 0.25% to 1.0%, combined with accommodative access to finance, resulted in heightened competition for assets, driving the total value of commercial and industrial property sales to $13.4 billion.

Over the subsequent 12 months, the OCR increased to 4.75% and remained on an upward trajectory. This saw investors adopting a more cautious approach, resulting in a significant slowing in activity, with the value of transactions falling to a provisional $5.8 billion*.

Transaction counts and annual sales values retreat from highs

When analysing sales by sector, industrial property was the strongest performer with 1,400 sales generating a total sales value of $2.84 billion, just under 50% of the commercial and industrial market’s annual figure.

Sales of retail properties comprised almost a quarter of the annual total by value at $1.3 billion. This was the highest share of total sales recorded by the sector since 2017. The total value of office sales at just under $893 million comprised 15.5% of the total, down from the sector’s 10-year average of 21.8%. This data highlights the ongoing confidence in the industrial sector’s demand, supply and income return drivers, greater focus on an office premises’ location and quality in a changed demand environment, and the retail sector’s longer term recalibration and transparency in performance metrics.

Trends mirrored across other asset classes

The reduction in commercial and industrial sales activity mirrors trends seen within the residential sector. Real Estate Institute of New Zealand (REINZ) data shows that in the 12 months to March 2022, the total value of residential sales nationally stood at $84.16 billion. By March 2023, the annual figure had retreated to $56.41 billion. Given the rise in the number of industry participants indicating a bottoming out in residential sales declines, this would also suggest that the end of declines in sales activity within the commercial and industrial sector is also imminent.

Outlook

Looking at the prospects for the remainder of 2023, it is likely that activity will increase from the levels witnessed in the first quarter. Over the last decade, first-quarter sales have comprised a smaller proportion of the annual total than the other quarters every year, with the exception of 2022.

Sales in the first three months of the year have generated an average of 16.5% of annual sales by value. As previously stated, the decline in sales activity has been driven by the rapid rise in interest rates. Investors have chosen to adopt a cautious approach given the uncertainty regarding the level at which interest rates would peak.

The stabilisation of interest rates and the expectation of future decreases are likely to underpin an increase in investor confidence and an upward trend in transactional activity.

*The lag in reporting of sales will result in total sales values being upwardly adjusted.